With the Omnibus proposal aiming to reduce reporting burden[1], the European Commission (EC) also announced its plan to quickly streamline, simplify and clarify the first set of European Sustainability Reporting Standards (ESRS).[2] EFRAG has received an official mandate to revise the first set of ESRS by the EC which asked for an innovative process to revise the standards and deliver the technical advice by 31 October 2025[3].

Accountancy Europe has been involved in every step of the first set of ESRS development. Throughout this process, we have highlighted challenges especially with regards to the requirements’ granularity and key concepts’ application.[4] Similarly, we have flagged the exceptionally high time pressure under which the first set of ESRS were developed, which affected the due process followed.

We acknowledge the need to improve the ESRS by providing more clarity and reducing granular requirements. We also believe a robust standard setting due process is essential to legitimise the standards in practice as it leads to higher quality and easier implementation. Due Process is a key principle in standard setting as noted in our paper Standard setting in the 21st century (2017).

Legitimacy

Independence

Transparency

Public accountability

Due process

Balanced membership

However, we acknowledge that under the current exceptional situation, the ESRS need to be improved quickly to continue to be fit-for purpose.

Based on our principles and acknowledging the political challenges, we provide suggestions to help EFRAG and the EC design an innovative process to revise the ESRS within an extremely tight deadline.

We strongly believe the rushed due process of ESRS set 1 has contributed to the implementation challenges. The consultation period was short, there was no field-testing, key part of the standards changed in each step of the process, and there was no time between finalisation and the effective date. EFRAG and the EC should learn from this experience to avoid creating further confusion in the market. Constant changes in reporting requirements increase costs, it is therefore important that any revision leads to more stable standards.

Accountancy Europe insists that public consultation and field-testing should be “non-negotiable” parts of the due process. We call on EFRAG and the EC to design a process that actively includes stakeholder feedback.

Public consultations should consist of clear, specific and targeted questions to stakeholders, and provide an adequate feedback period depending on the type of amendments (see our suggestion below on “less complex” vs “complex”). In addition, field-testing should feed properly into the final deliverables, by using the experience of the first reporters or by target-testing the proposals.

EFRAG has been given 7 months to deliver its technical advice, which makes a normal due process impossible to run. In designing an innovative but fit-for-purpose process, we invite EFRAG to consider a project task force approach to maximise time efficiency. This process should focus on practical aspects and prioritise feedback from first year implementation.

Lastly, in such a short timeframe, timely communication to the market and updates to stakeholders at every stage will be paramount.

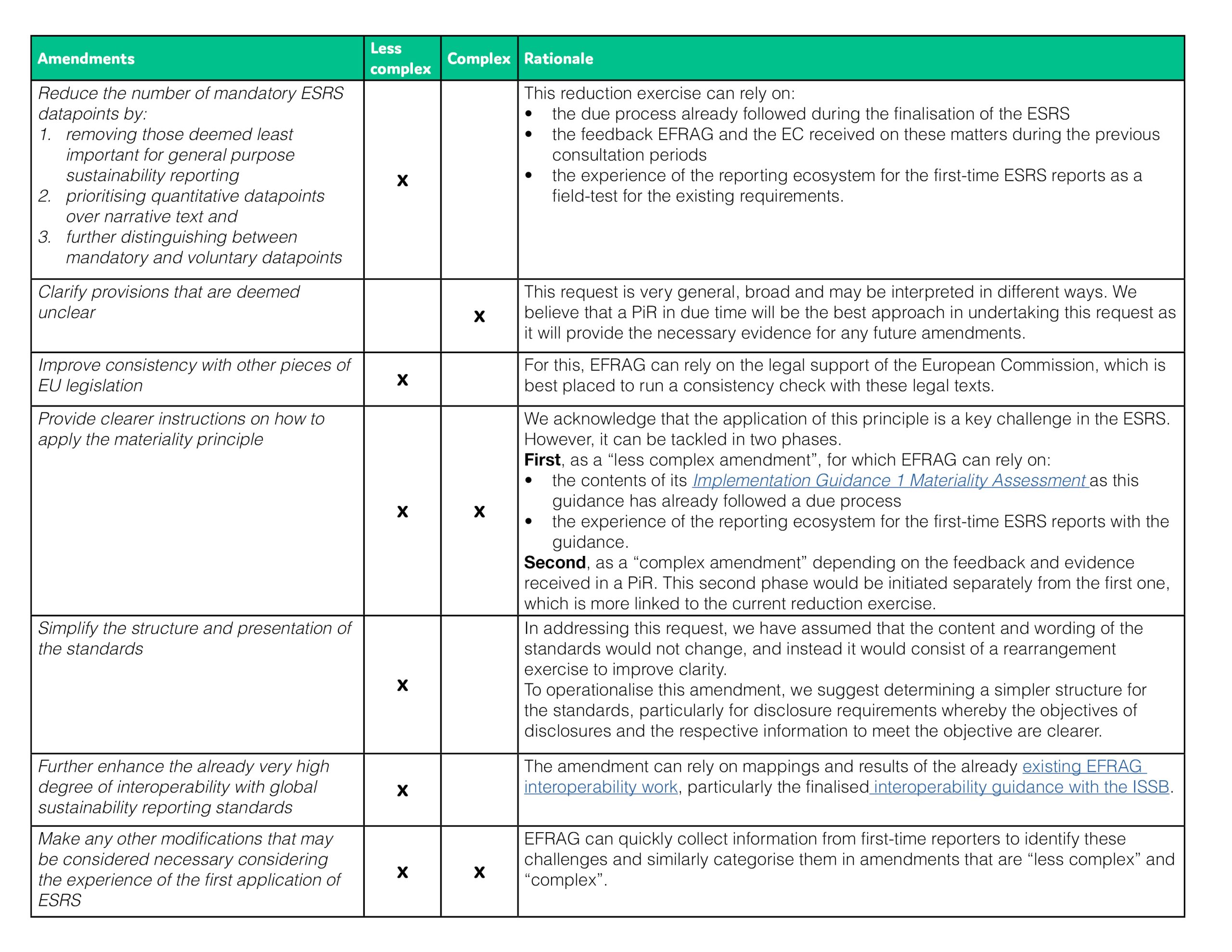

The EC’s list of targeted reviews could be split into two groups based on the amendment complexity, with each group following a different due process.

The “less complex amendments” should target the standards’ existing contents. These amendments can build on EFRAG’s existing guidance work and rely on the respective due process followed, provided that it includes the “non-negotiables”. In this case, it could accommodate a shorter consultation period. The experience of the first wave of reporting could serve as the “field test”.

The “complex amendments” should consist of changes, such as additions to the standards that have not gone through any previous public consultation. These amendments should go under a more thorough due process, including a longer consultation period as well as a targeted field-test for any new text to the standards. Such changes may be best suited for a future post-implementation review (PiR) rather than this reduction exercise.

Below, we outline an idea to group the EC’s amendments from the Omnibus proposal recitals. Accountancy Europe stands ready to contribute to the simplification of set 1 ESRS.

[1]Please refer to our factsheets for more information on the proposals: Omnibus explained: key changes to CSRD, Omnibus explained: key changes to CSDDD, Omnibus explained: key changes to CBAM.

[2] Please refer to our factsheet Omnibus explained: key changes to sustainability reporting standards for more information on the changes related to the standards.

[3] The EC acknowledges that this target date may change depending on when the Omnibus proposals will enter into force.

[4] Please refer to our publications ESRS perspectives: Materiality assessment, ESRS perspectives: Value Chain, ESRS perspectives: ESRS perspectives: process & development, ESRS perspectives: Interoperability.