14 July 2026 — Publication

Insights, trends and resources

Private Equity (PE) refers to investment by third-party investors in private companies, aiming to generate returns through growth and operational improvements. Recent technological developments and market competition have led to increased PE investment in accountancy firms, attracted by their recurring revenues and growth potential. Third party investment in accountancy firms can come from different sources like staff or even family shareholding, long-term passive investors like pension funds, public listings, but currently private equity is the most prominent external investment in the sector.

This page provides an overview of our research on PE and third-party ownership more broadly, including resources from our members and international organisations.

For more information on PE contact Endrin Bitraj: [email protected].

The accountancy profession has traditionally been characterised by partnership structures and organic growth. Firms have expanded through internal development, long-term client relationships, and reputational strength, rather than external investment or acquisition.

However, fast-moving technological developments, digitalisation and increasing competition have led firms to invest more heavily to remain competitive. At the same time, third party investors, and especially PE investors have identified opportunities to invest in accountancy firms, attracted by their recurring revenues, cash flows and growth potential. There has been a notable increase in PE investments in the accountancy sector in recent years.

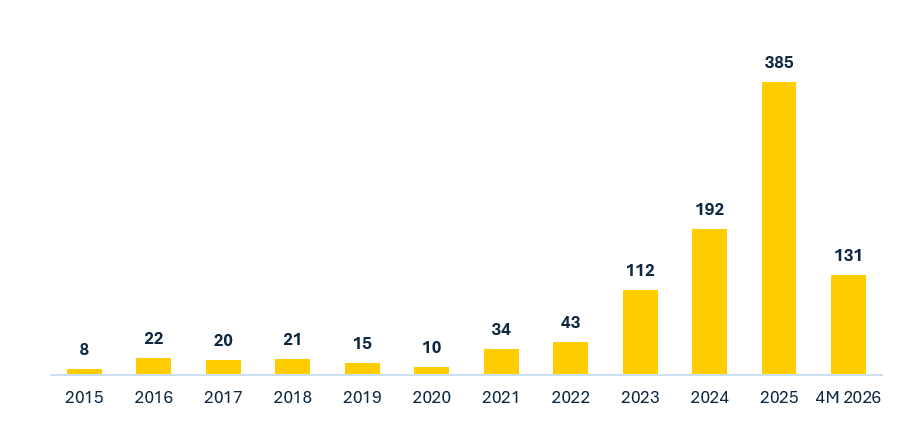

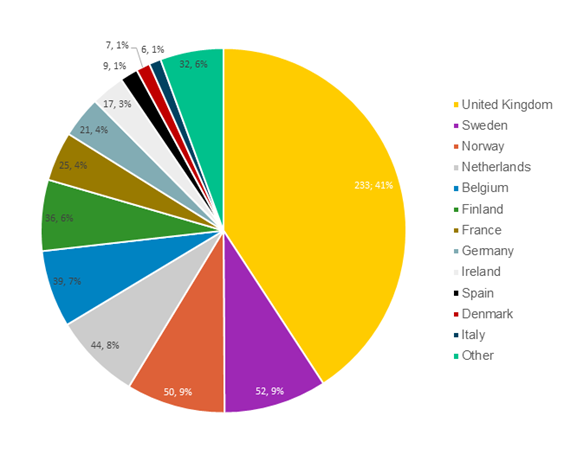

PE investment in the European accountancy sector has grown significantly over the past decade. Accountancy Europe gathered and analysed public data on PE investment transactions related to accountancy firms across Europe between 2015 and April 2026.

More than half of the deals (60%) involve primarily local accounting, tax, and advisory firms, while approximately 40% of the deals are in firms that also provide audit and assurance related services.

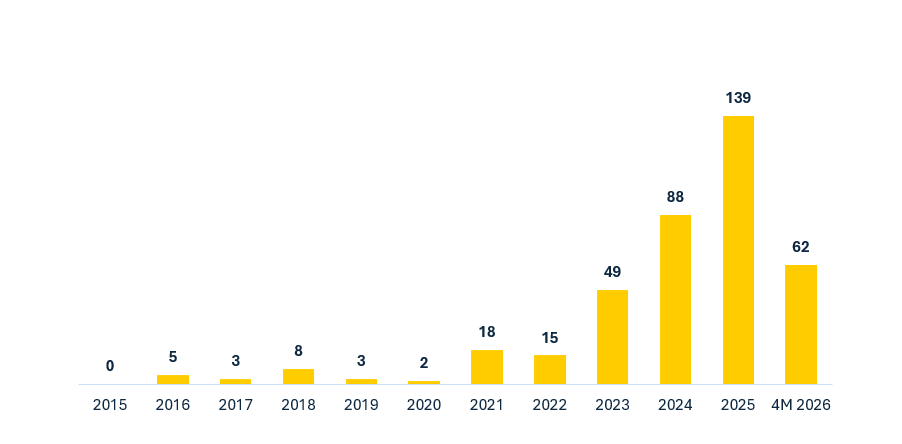

A similar trend can be observed for audit and assurance firms:

This indicates that growth in private equity activity is continuing across the audit and assurance sector.

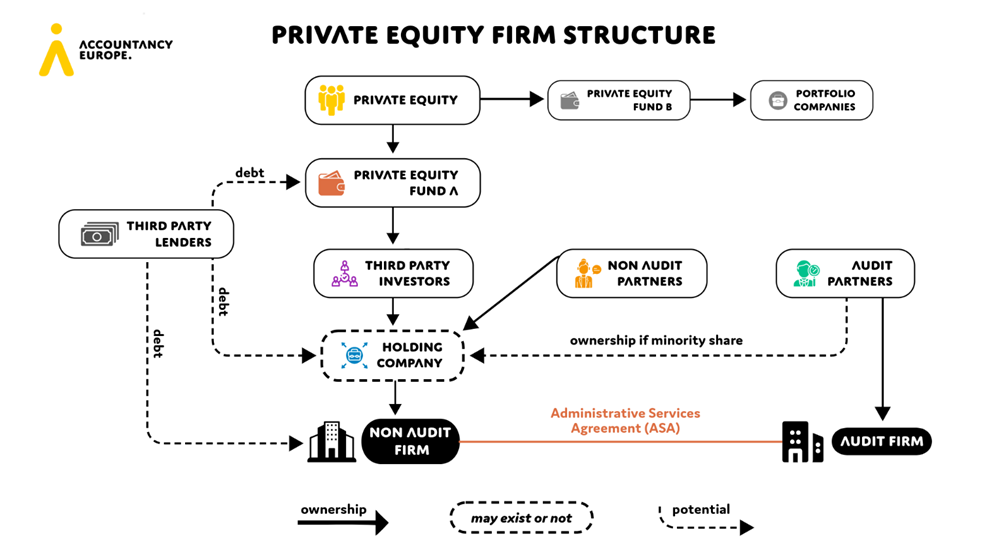

A PE fund ordinarily invests in an accountancy and audit firm that undergoes legal restructuring into two distinct entities: an audit firm and a non-audit firm. The non-audit firm usually provides professional services and resources to the audit firm under an administrative services agreement (ASA).

Third party ownership is on the rise. Models such as PE are becoming more common across Europe and are reshaping the accountancy and audit profession. This trend comes with both opportunities and challenges, from growth and innovation to questions about independence, governance and audit quality. The debate is therefore not about whether third-party ownership will shape the future of the profession, but how its implications will be managed in practice.

Accountancy Europe does not take a position against or against third-party ownership. We bring together different perspectives so that policymakers, regulators, investors and the profession can have an informed and constructive dialogue.

Private equity in European accountancy and audit firms - an update on market activity from January 2025 to April 2026 (publication, July 2026)

Beyond private equity: third party ownership in the accountancy and audit sector (publication, November 2025)

Beyond private equity: third party ownership in the accountancy and audit sector (summary, November 2025)

Private equity investments in accountancy firms (publication, June 2025)