25 February 2026 — Publication

Trust and integrity: the role of corporate ecosystem actors in preventing greenwashing

The term ‘greenwashing’ is relatively new, but the underlying conduct is not. Sustainability information is key to capital allocation and stakeholder decision-making and demand for it will persist. With lighter regulation due to the latest changes under the ‘simplification agenda’, ensuring good governance and clarifying the roles of corporate ecosystem actors is more important than ever. Deepening understanding and guidance in this area remains critical.

Access the full publication.

Greenwashing can range from negligent, to reckless, to fraudulent conduct. Detailed descriptions await in our annexed document.

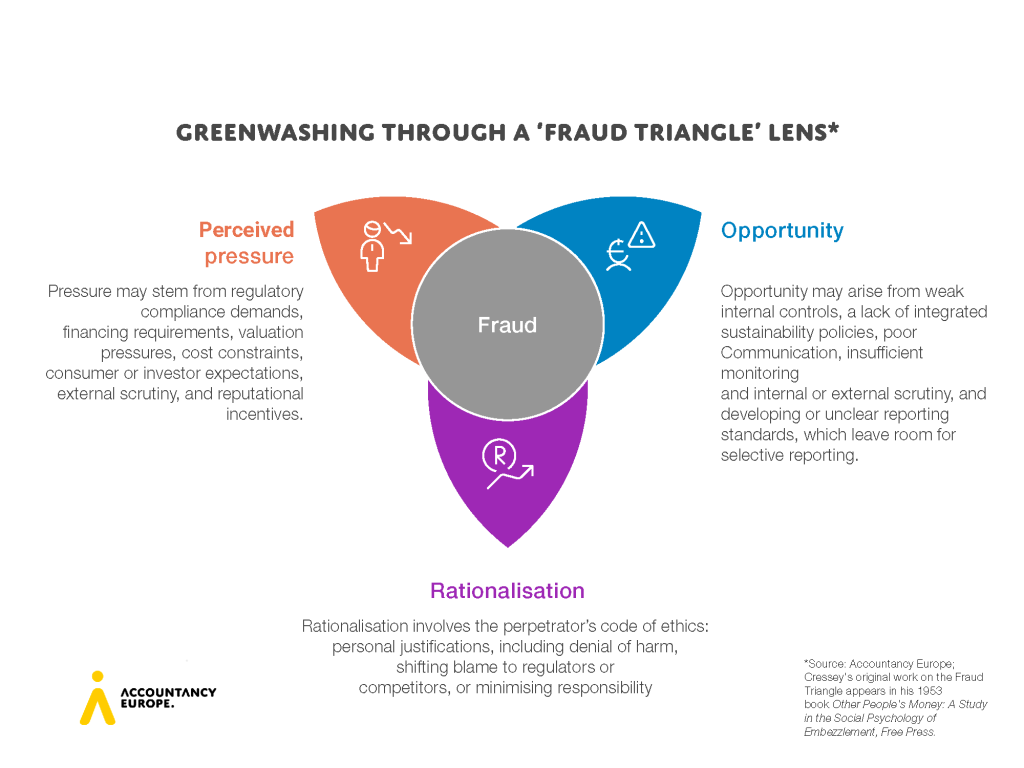

It is worth considering Cressey’s ‘fraud triangle’ to assess when fraudulent greenwashing is likely to occur. The ‘fraud triangle’ identifies three factors that drive fraud: perceived pressure, opportunity, and rationalisation.

Access the full annex.

Greenwashing often arises from unclear definitions, regulatory gaps, excessive rules, or unethical corporate behaviour. Beyond fines and litigation, the erosion of stakeholder trust is one of the most damaging consequences. This can lead to misallocated capital, compromised ability to drive sustainability, and long-term reputational damage.

The publication aims to demonstrate to policymakers that mitigating greenwashing risks requires a systemic approach. We examine how different actors in the corporate ecosystem can identify and mitigate greenwashing risks, clarifying how each contributes to safeguarding the integrity of sustainability disclosures.

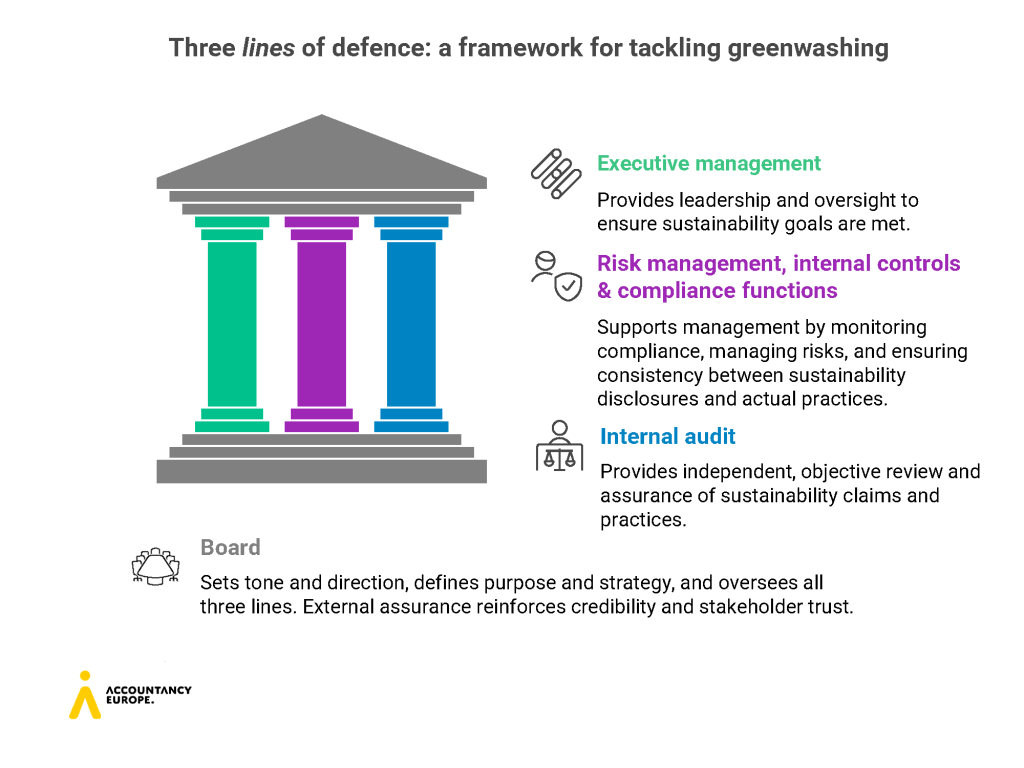

We explore how preventing greenwashing is a shared responsibility, structured around the Three Lines of Defence model to clarify accountability.

Boards exercise effective oversight by challenging and supporting management to implement processes and controls that ensure sustainability claims are accurate, consistent with the company’s conduct and objectives, and not misleading to stakeholders.

The CEO and executive management collectively form the first and second lines of defence. They manage day-to-day risks, including those related to sustainability and greenwashing, and oversee risk management, compliance, and internal control frameworks. They are responsible for ensuring sustainability narratives are balanced, credible, and aligned with actual performance, and that sustainability commitments are operationally supported, adequately controlled, and subject to appropriate assurance processes.

The Chief Sustainability Officer (CSO) role provides accountability and coherence in managing sustainability-related opportunities and risks, though it is not yet universal. The CSO plays a key role in managing greenwashing risks by ensuring sustainability commitments are credible, evidence-based, and aligned with business conduct and stakeholder expectations. Through regular interaction with executive leadership and board committees, the CSO helps to strengthen oversight and guard against misleading disclosures.

The CFO’s role is expanding beyond financial reporting to include sustainability disclosures. They are increasingly seen as gatekeepers, responsible for ensuring that corporate statements are accurate, verifiable, and aligned with actual performance across both financial and sustainability contexts. CFOs translate sustainability metrics into financial terms, integrate ESG data into enterprise-wide planning, and ensure robust systems underpin both financial and sustainability reporting.

Effective risk management, as part of the second line of defence, is central to preventing and mitigating greenwashing, ensuring risks are identified, assessed, and monitored like other material risks. Compliance professionals support this by ensuring disclosures comply with laws, regulations, and internal policies, and that external communications align with internal processes and decisions. In this way, risk management, internal controls, and compliance act as a critical safeguard, ensuring sustainability claims are credible, evidence-based, supported by robust systems, and enhancing the verifiability and assurance of sustainability reporting.

As part of the third line of defence, internal auditors help ensure a credible sustainability control environment. They evaluate the design and effectiveness of sustainability-related internal controls, identify inconsistencies between policy and practice, assess reporting maturity, and support compliance with applicable frameworks. Their work strengthens assurance and governance processes, helping boards and management address greenwashing and other sustainability-related risks.

Audit committees provide independent oversight of management and assurance functions, including risk management, internal controls, internal audit, and reporting integrity. Their role has expanded in the sustainability context, requiring greater scrutiny of ESG data, reporting frameworks, and the internal processes that underpin them. By applying the same rigour to sustainability disclosures as to financial reporting, they help ensure claims are credible, evidence-based, and supported by robust systems, controls, and assurance processes.

External assurance enhances credibility of sustainability reporting. In an assurance engagement, assurance practitioners will consider the overall business environment of the company. They use a risk-based approach, focusing on potential biases, omissions, or overstatements that could indicate greenwashing. Fraud risk factors, i.e. pressure, opportunity, and rationalisation, are considered, along with the maturity of sustainability reporting controls. The public assurance report communicates conclusions on the reported sustainability information. When relevant, significant issues, including greenwashing risks, may be reported privately to management or the board.

Greenwashing rarely stems from a single actor; it reflects systemic weaknesses, fragmented governance, and unclear accountability across the corporate ecosystem. Preserving trust requires moving beyond ‘virtue signalling’ toward a holistic framework where sustainability claims reflect real performance and shared responsibilities across all lines of defence. Policymakers must ensure clear definitions, coherent regulation, and aligned oversight to support a sustainable transition built on credible, reliable information.